Scope 3 Emissions: the Catalyst for Change in the Logistics Sector

By Charlie Bell, Propositions Lead, VEV

The logistics industry stands at a crossroads, facing growing pressure to embrace sustainability but no clear answer on when or how to respond. While many logistics companies are focused on reducing their direct emissions and meeting government net zero targets, a new challenge looms on the horizon: Scope 3 emissions, an aspect of carbon accounting poised to become a major driver of change.

Understanding scope 3 emissions: a hidden opportunity

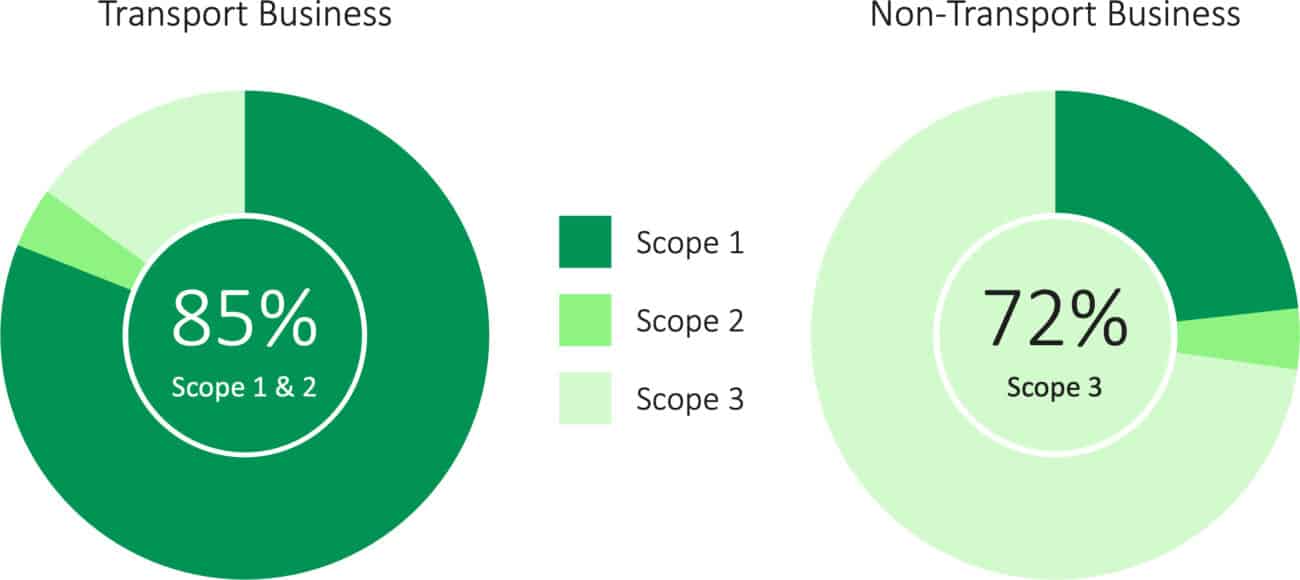

Logistics businesses might assume that their primary concern lies with Scope 1 and 2 emissions – those directly produced by their operations and energy use. According to CDP research these Scope 1 & 2 emissions typically account for 85% of a transport business’s total footprint. However, this perspective misses a crucial point: emissions generated by logistics companies are part of their customers’ and the broader supply chain’s Scope 3.

Conversely, according to the same CDP research, a non-transport business’s total output is dominated by their Scope 3 emissions – 72% – with transport alone contributing 5-20% of the Scope 3 total. For logistics providers, this means that while they may not directly account for these emissions, they do play a pivotal role in their customers’ emissions targets. This represents both a challenge and an opportunity for logistics companies willing to adapt and innovate.

Decarbonisation and regulatory pressure on transport and logistics

While intense customer pressure for sustainable logistics solutions isn’t widespread today, it’s rapidly emerging and set to become a major force in the near future. Evidence of this emerging trend is already visible.

A recent study found that 64% of shippers are beginning to assess freight providers against carbon compliance schemes[1]. This indicates a growing awareness and concern about Scope 3 emissions among the customers of logistics suppliers.

As large brands set ambitious targets for reducing their Scope 3 emissions, they will increasingly look to their logistics partners to help meet these goals. Some major UK brands and retailers have already set targets under the Science Based Targets initiative (SBTi). For example:

- Tesco is targeting a 55% decrease from its 2019 levels by 2030.

- Marks & Spencer has set a 55% reduction target by 2030.

- John Lewis has promised a 42% reduction in emissions from purchased goods and services, and use of sold products, by 2030.

As they look to meet their Scope 3 targets, brands will cascade the targets down the supply chain, placing new pressures on logistics providers to offer low-emission services.

Addressing fleet emissions – fleet electrification

The most effective path for logistics providers to achieve meaningful reductions in Scope 3 emissions for their customers is through tackling fleet emissions.

This primarily involves exploring options for fleet electrification or sustainable fuels. While other sustainability initiatives can contribute to emissions reduction, addressing the emissions from vehicles will have the most significant impact.

Logistics businesses without clear, milestone-driven plans to reduce their fleet emissions risk losing business to more proactive competitors. Gone are the days of promises and office recycling initiatives going into the ESG section of a tender.

Proactive vs. Reactive: a strategic choice

Logistics companies now face a critical decision: wait for customer and regulatory pressure to force changes or proactively prepare for the inevitable shift towards net zero. Those who choose to act now, by addressing their fleet’s emissions, will position themselves as industry leaders and gain a competitive edge in an increasingly environmentally conscious market. They will have the opportunity to learn, shaping the market and technology.

Those who wait won’t have the same luxury – needing to accelerate up the learning curve to meet upcoming regulations and respond to new customer demands.

Developing green corridors for transport and logistics routes

Even logistics companies who are aware of this pressure might feel they are in a chicken-and-egg situation. Prevailing industry wisdom suggests that vehicle ranges need to improve and public charging networks need to develop further to electrify road freight effectively. While these changes are indeed necessary for system-wide decarbonisation, it’s crucial to recognise that specific routes can be moved to net zero today.

Frequently travelled routes with the right mileage and access to charging at a depot and/or destination can be electrified today, creating ‘green corridors’ – low-emission transportation routes.

The European Federation for Transport and Environment estimates that 65-75% of Britainʼs rigid HGVs and 30-35% of articulated HGVs can move to electric without reliance on public charging infrastructure.[2]

Provided they have sufficient power available at a depot, logistics fleets don’t need to wait for public infrastructure to develop to make their first steps.

This approach allows businesses to meet growing customer demands for sustainability and make progress on Scope 3 reduction targets, all while differentiating themselves in a market where misconceptions about costs and infrastructure are slowing wider adoption.

Anticipate change for future success

The hidden wave of Scope 3 emissions is set to become a major catalyst for change in the logistics industry. While the pressure may not be overwhelming today, the trends are clear: customers will soon demand significant reductions in their supply chain emissions to meet their Scope 3 targets.

Logistics companies that recognize this emerging trend and take proactive steps to address their fleet emissions will be well-positioned to defend their core business and capture new opportunities. Moreover, they will be the pioneers leading the industry towards a more sustainable future.

As the logistics sector continues to evolve, staying ahead of sustainability trends will be crucial for long-term success. By addressing Scope 3 emissions now, companies can not only meet future regulatory requirements but also play a pivotal role in shaping a greener, more efficient logistics landscape.

[1] https://engage.transporeon.com/rs/307-ROC-257/images/Report_Decarbonization_Freight_Report.pdf

[2] https://www.transportenvironment.org/uploads/files/2023_05_TE_study_summary_HGVs_road_net_zero.pdf